Biden Tax Hike: What Fiscal Advisers Are Telling Loaded Purchasers

5 min readPresident Joe Biden’s proposal to about double the funds-gains tax for the wealthy has place fiscal advisers in the strange placement of performing as aspect therapist and section fortune teller. Frantic calls are coming in from purchasers surprised to see that what they’d dismissed as rhetoric from the 2020 election campaign has come out this 7 days as concrete White Dwelling proposals.

Advisers are telling them to retain tranquil, but they’re also counseling to prepare for action—bringing forward prepared asset product sales, shedding inventory, reallocating investments, and even restructuring cash flow. “Don’t do anything drastic just nonetheless,” Ed Reitmeyer, a lover at accounting company Marcum LLP, is telling his clientele. “The environment is not in excess of simply because of a bigger funds-gains tax level.”

President Joe Biden speaks throughout a joint session of Congress on April 28.

Melina Mara/The Washington Publish/Bloomberg

It may perhaps not be around, but it would be adjusted. For men and women and partners earning additional than $1 million, Biden is proposing to maximize the tax fee on revenue realized when an asset is marketed to 39.6%. He also needs to conclude a tax crack that wipes away taxable funds gains at demise, allowing for households to escape taxes on appreciated assets when they’re inherited.

The present funds-gains tax price is 20%, just one of the most affordable ranges in the 100-12 months background of particular tax charges for investments. Relying on how the legislation shapes up in the coming months in Congress, the richest Us residents can anticipate bigger tax expenditures in the long term. The White Residence states the new top cash-gains rate—43.4% when like a surtax to assistance fork out for the Very affordable Care Act, or Obamacare—applies to .3% of taxpayers, or about 500,000 households.

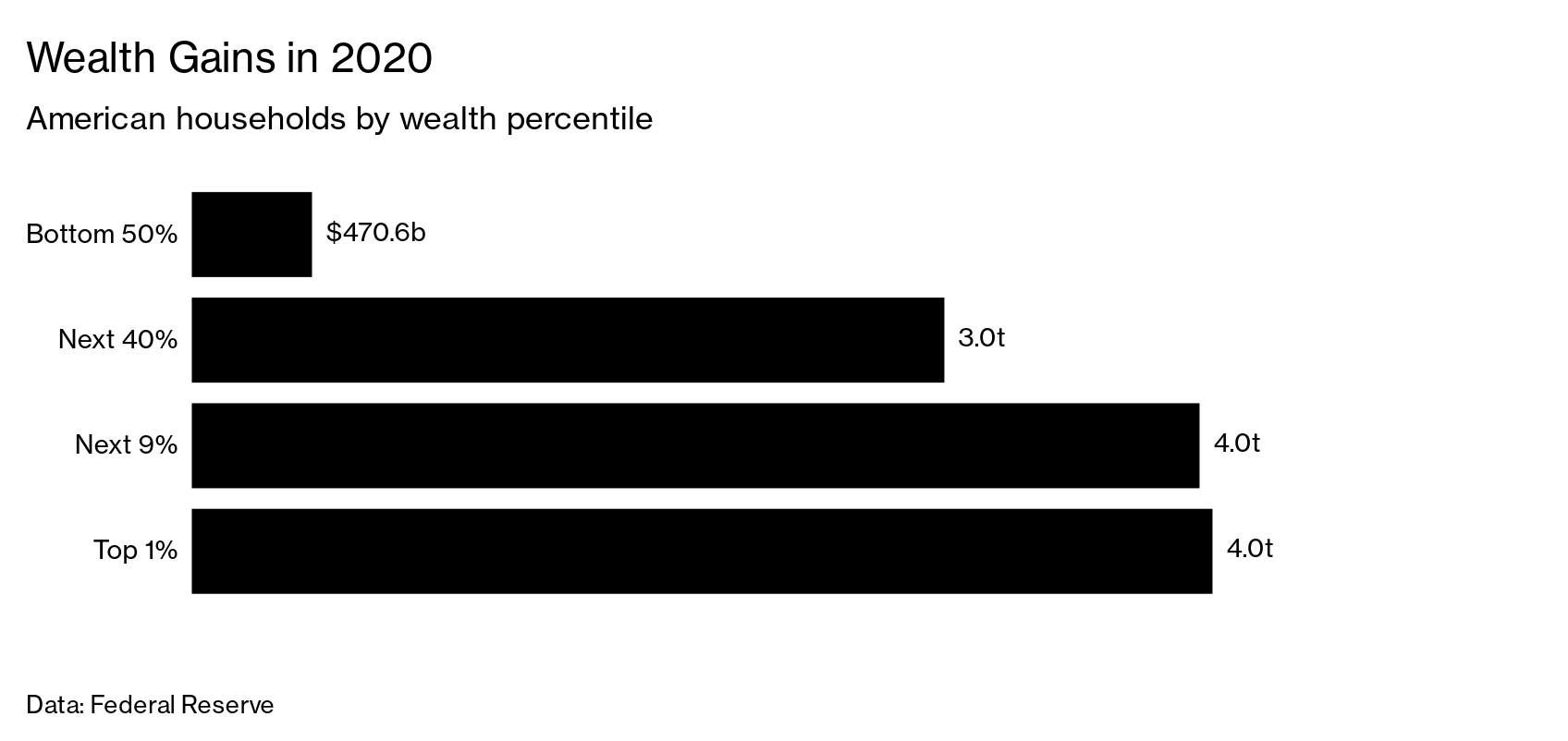

Prosperity Gains in 2020

American households by prosperity percentile

Knowledge: Federal Reserve

Though fairly modest in range, these taxpayers loom huge in their share of prosperity. Seeking at only a a little much larger slice, the richest 1% of households are sitting down on as significantly as $1.5 trillion of unrealized funds gains on equities, according to calculations by Goldman Sachs Group Inc.

“Of program clients are concerned,” says Chris Pegg, senior director of prosperity planning for Wells Fargo Wealth & Financial investment Management. In particular concerned: individuals planning large taxable transactions this kind of as gross sales of corporations, he says. The uncertain route for the laws does not dispel the angst, possibly. “You seriously just cannot explain to what’s coming, and still you have to system in any case.”

Cash-gains taxes are compensated only when an asset is bought, so some buyers could system to keep on indefinitely and potentially bypass any increased charges below Biden if Republicans earn back again energy in Congress and lower them in the upcoming. Advisers are counseling all those needing to shift faster, or who are a lot less optimistic about long term tax cuts, to consider about rushing up transactions or to glimpse at techniques to limit the bite.

“We might be in a place to persuade our consumers to promote down some of these holdings and spend funds gains at a lessen amount before all those tax rates double,” suggests Tony Roth, main expense officer of Wilmington Believe in Financial commitment Advisors Inc. Talking on Bloomberg Tv previous 7 days, he flagged unrealized gains on tech shares in specific as an asset ripe to take into consideration locking in gains.

But some advisers are obtaining consumers hesitant to offer, immediately after many years of becoming instructed to do just about anything to prevent triggering a taxable occasion. “We have 1 of the lowest capital-gains premiums in heritage proper now, but my clientele nevertheless never shell out funds gains. They however never promote inventory. They never like using any gains,” claims Austin Frye, a prosperity adviser in Miami.

There is some possibility in performing much too soon. Biden’s proposal is an opening bid. Democrats in Congress are previously reshaping the strategy, and any proposal has to very clear razor-slim margins in the two the Property and Senate. In all probability, any closing legislation will be additional reasonable and contain some mix of lessen costs or a lot more carve-outs than what is in-depth in the Biden system.

Much more alarmingly for the wealthy, Congress also has the power to make the variations retroactive, to the start out of 2021 or even previously. But indicators are that is not the White House’s choice. “Retroactively is usually not favored,” claims Todd Simmens, a former legislative counsel to the Joint Committee on Taxation, who now will work for accounting business BDO. “If folks are arranging for some adjustments, it would be harmless and prudent to presume that the adjustments are successful in January 2022.”

1 tactic for buyers who are persuaded their existing holdings will hold rising in benefit: selling, shelling out the tax at today’s amount, then buying the asset again. This program of motion sets a new, better invest in selling price that minimizes any foreseeable future levy, states Todd Morgan, chairman at Bel Air Expenditure Advisors in Los Angeles. That technique could perform perfectly for an asset these types of as Tesla Inc., whose inventory has enhanced just about 700% considering that the start of 2020, or Bitcoin, which was just about worthless a 10 years in the past but now tops $50,000.

“Wealthy individuals and traders normally have the potential to maintain for as lengthy as they want” and generally borrow versus their portfolios if they require cash for present-day use, says Alison Hutchinson, taking care of director at Brown Brothers Harriman & Co. If the procedures alter, nevertheless, investors may decide to sell just before the alterations go into impact.

One particular other new dilemma the rich could experience is increased IRS scrutiny, a thing that has guidance from each Democrats and Republicans. Biden wants $80 billion for the IRS to bolster enforcement in the coming ten years.

The most evident way to steer clear of larger funds-gains charges is to continue to keep cash flow less than $1 million in any provided yr. Marya Robben, an estate-planning attorney at Lathrop GPM in Minneapolis, claims her executive consumers might want to shift much more profits into deferred compensation plans. Pegg at Wells Fargo notes that sales of residence or non-public corporations could be structured in means that buyers shell out sellers around a interval of several years, spreading out that profits.

As constantly with difficult regulations, it pays to pore around the fine print. Variations “will be built with protections” for household-owned firms and farms, allowing “heirs who continue to operate the business” to prevent paying out taxes, a White House truth sheet suggests. “It will be intriguing to see how you define these things,” Hutchinson states.

If the tax-hike legislation does move this calendar year, rich investors could have only a few of months—or even a handful of months if the negotiations drag on lengthy enough—to respond in advance of the variations take influence. “You may want to accelerate income. You could possibly want to defer deductions to a time when they would be additional valuable,” Pegg says. “If you imagine you can get the deal done, get the deal accomplished.” —With Tom Keene

Examine following: How Bill Hwang of Archegos Funds Misplaced $20 Billion in Two Times